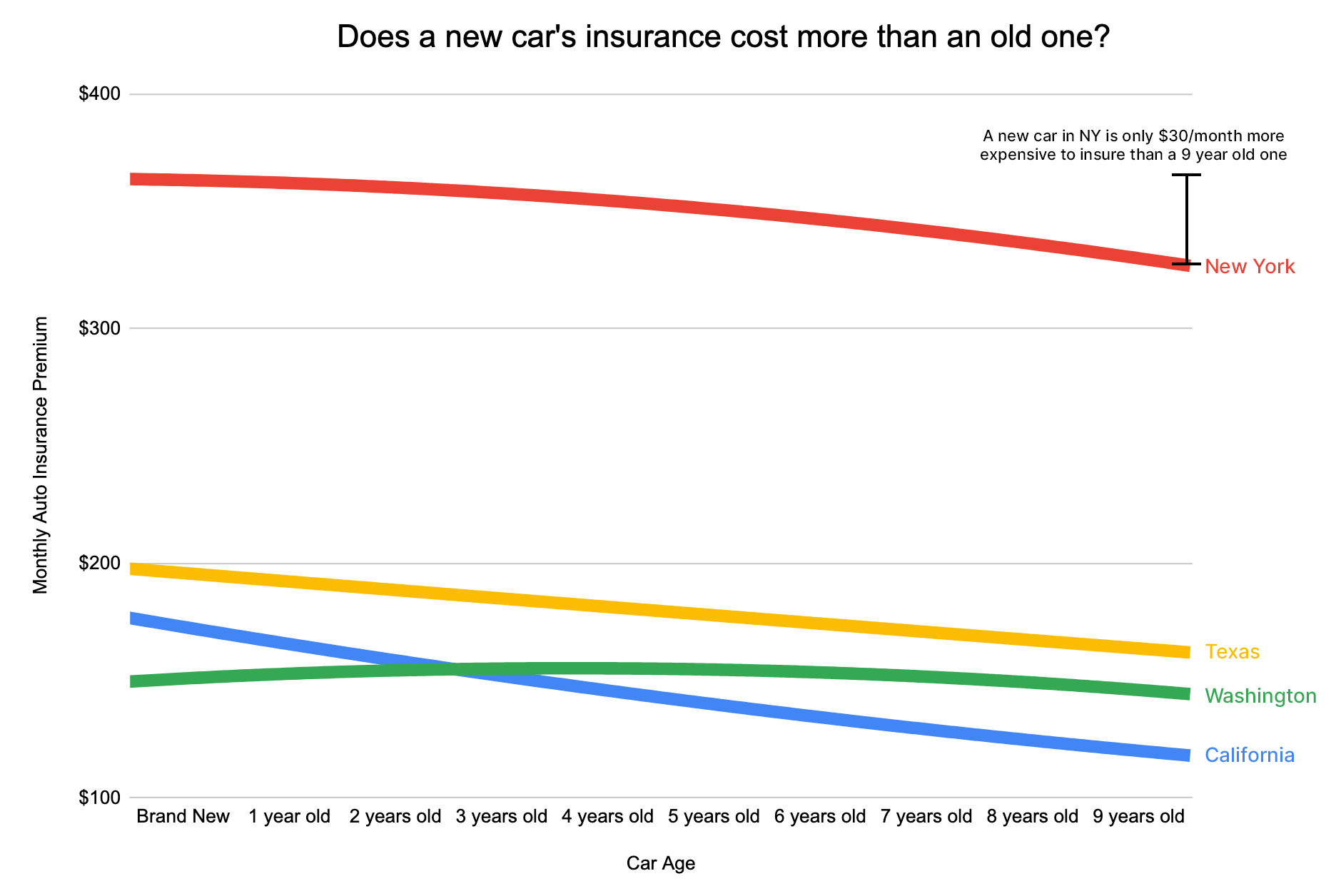

Car Insurance / Types of Car Insurance / MedPay

Reviewed by: Max Cho, Licensed Insurance Broker NPN 20377411

Types of Car Insurance: Minimum Required Insurance / Liability Coverage / Uninsured Motorist / Collision / Comprehensive / PIP / MedPay

Despite its name, it actually covers a great deal more than just your direct healthcare costs. Typical healthcare costs include medical payments, deductibles and copays, doctor and hospital visits, ambulance transportation, diagnostic tests like x-rays, and surgery. MedPay also covers dental treatment, chiropractic treatment, and funeral expenses.

Do I need MedPay?

MedPay is required in the following states: Maine, New Hampshire (if you have car insurance), and Pennsylvania.

Why you might want MedPay anyway

MedPay isn’t available everywhere, so assuming it’s available where you live, here’s how to think about it.

MedPay exists to help you pay medical-related expenses related to an accident, right away.

You don’t even need to be in your car when you’re involved in an accident caused by someone else (you could be a pedestrian or even on a public bus).

MedPay covers you (and your family members) if you’re hit by a car on foot, riding a bike, or traveling as a passenger in someone else’s vehicle. This extended universe of coverage is valuable, especially if you live in an urban area or frequently engage in those activities.

How MedPay is different from health insurance

MedPay covers your own medical bills in an accident, but it often covers more than just the things your health insurance covers, such as dental treatment, chiropractic treatment, and funeral expenses. You can use MedPay to cover your deductibles and copays.

MedPay also covers other people! While health insurance only covers you, and your household members (if they’re on your family plan), MedPay can cover your passengers, or pedestrians and cyclists whom you injure in an accident.

Some health insurance policies exclude car-related injury coverage and MedPay can make up the difference. If your health insurance does cover car crashes, your health insurance company and your car insurance company are probably going to squabble about who pays for what.

How MedPay is different from Personal Injury Protection (PIP)

If you live in a “no fault” state you’re probably required to have PIP. Some states where you are required to have PIP you are not allowed to also have MedPay, but in some states where PIP is optional, you can also opt in to MedPay. Check your local rules.

PIP sounds pretty similar to MedPay, but the best way to think of MedPay is as a (somewhat limited) extension to PIP, with some extra benefits.

While MedPay typically covers medical-related expenses, PIP also covers some of the other costs that might arise after a crash. Some of these expenses include: Lost income if you can’t work due to injury, replacement services (like childcare) for when you can’t do things yourself related to injury, psychiatric treatment, physical and occupational therapy, and rehabilitation.

PIP often has a deductible of its own, while MedPay does not.

Note: despite what we have seen on some other websites, there is no nationwide legal prohibition against having both MedPay and PIP. Some states may limit whether you can have both, but some insurers may have their own policies either allowing or restricting having both coverages.

How much MedPay coverage do I need?

Unfortunately MedPay usually has fairly strict coverage limits, with a maximum of $10,000 in many states (though more is available in California and State Farm offers policies up to $100,000 according to a law firm’s website). As coverage is limited, MedPay is fairly inexpensive (especially when compared with the cost of health insurance).

If you live in Michigan, you don’t need MedPay. Michigan is a “no fault” state and it’s the only one with no limit on medical expenses as the Michigan Catastrophic Claims Association (MCCA) kicks in when you reach the coverage limit.

If you have PIP, you probably don’t need MedPay, but if you can afford it (a relatively small amount), it’s not a bad “extra” to help cover out of pocket expenses after a car-related injury — including when you’re not even in your car.

If you have health insurance, your MedPay coverage should equal that of your health insurance deductible. If your Maximum Out of Pocket is higher, get coverage for that amount.

If you don’t have health insurance, MedPay coverage on your car insurance is a really good idea, and you should buy as much as you can afford. So is PIP for that matter.

Want to find the best insurance? Need help?

Coverage Cat shops for you. We search across dozens of major insurers and use data science to compare millions of real quotes. The result? The best combination of policies, coverage, and price for your personal financial situation.

Our promise: